|

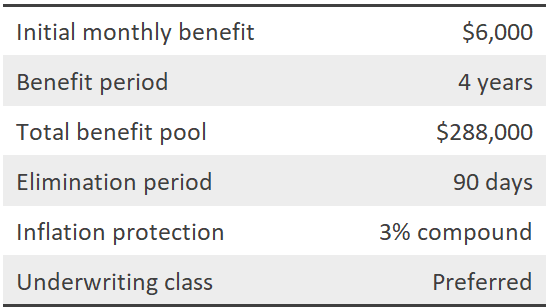

In our previous post, we covered the basics of long-term care insurance. Today, we want to look at pricing and alternative products to traditional long-term care insurance.  PRICING Okay, let’s look at the rates for the same policy we discussed in the previous post at various ages for nonsmokers in good health. As a reminder, here are the basic policy features.  As far as pricing goes, the younger you are, the lower the premium. And premiums for females are higher than those for males. Furthermore, a couple applying together gets a discount.

Premiums are payable for life and is not guaranteed. So it can increase in the future. If you prefer a shorter premium payment period and be done with it, there is a product that allows you to pay premiums in one lump-sum or over 10 years. NONTRADITIONAL PRODUCTS: LIFE INSURANCE WITH A LTC RIDER So far, we’ve talked about the “traditional” long-term care insurance. This is normally what we think of when we mention long-term care insurance. But beyond the traditional option, you actually have two other product types you can consider:

If you’re young-ish, you probably wouldn’t be too excited about the prospect of planning for long-term care. And you definitely won’t be interested in making premium payments year after year for benefits you might not need for a half century or more. Half a century! Man, that’s a long time. But still, it’s prudent to plan for it if it makes sense in the grand scheme of things. If this is you, you might consider life insurance with a long-term care rider. This way, you get their life insurance coverage (which you probably need anyway) and build cash value. If you’re a parent and fortunate enough to make annual gifts to your child(ren), you might consider buying life insurance with a long-term care rider for your child(ren) in their 20s and 30s. if designed right, it can go a long way in helping them build a small nest egg for them in a tax-favored way without market risk. NONTRADITIONAL PRODUCTS: HYBRID PRODUCTS As for hybrid products, as the name might suggest, it’s a hybrid between long-term care and life insurance. Premium structures for hybrid products are often more flexible. You can pay in one lump-sum over 10 years, to age 65, for lifetime, and so on. And unlike traditional long-term care insurance, premiums are guaranteed to never increase. The question we often get asked is, “What if I pay make all these premium payments and die without every using the benefits?” Well, this may the product for you. With a hybrid product, there is a small death benefit should you never use long-term care benefits. What’s more, you can design a hybrid policy so you can recoup your premium payments if you decide to cancel the policy in the future. It’s generally subject to a vesting schedule, so you have to wait a few years before you can recover your full principal. In our next post, we’ll share with you what’s involved in underwriting and some sobering statistics. Comments are closed.

|

|

|